On a par with the continuous stream of headlines on worrying climate change impacts worldwide, we now also find daily news of advances towards decarbonization and climate action. From Court orders and corporate shareholders forcing big oil companies to address their emissions, to financial investors flooding the climate tech sector, not a day goes by that doesn’t include some indication of a decarbonized future. While there are good reasons not to feel too optimistic yet, it does look like this could be a transformative Climate decade.[1]

This essay will highlight significant action underway, specifically the rise of renewables, the market moves to join the energy transition, and the role of government, in particular China. The idea is that, together, these changes are part of what some are referring to as a “green vortex” of positive feedbacks that might finally move things in the right direction.

The Green Vortex

As described by Robinson Meyer, decarbonization isn’t best accomplished by directives but rather as the result of a positive feedback loop, in a self-accelerating process powered by technological change and financial incentives which can be thought of as a “green spiral” or “green vortex.[2] The key driver is profit, but industrial policy - both national and foreign - play a major part.

An instance of this process is what happened with wind energy: according to Greg Nemet, the rise of wind farms can be traced to the 1970s when, as a consequence of the oil crush, Denmark started providing seed investments for a homegrown wind industry, which ten years later found a market in California when the state began subsidizing large wind farms. Likewise, cheap solar energy is said to have largely emerged from the confluence of subsidies for solar panel factories in China, and Germany’s tariffs after 2010.[3]

Key to decarbonization now is the steady progression of clean energy technologies, the piecemeal, bottom-up investment, led on by government subsidies, foreign industrial policies, tax rebates and such incentives. A critical turning point in the process is when the companies that sell high carbon-content products start selling the substitute low or zero-carbon ones. This is the case of electric cars for example, which can turn the automotive industry from one opposing climate change regulations to one favoring them. Signs that this is happening are starting to show: Ford Motor Company, for example, recently announced that it’s planning to spend more on electrified vehicles than it does on internal combustion engine vehicles starting already in 2023.[4] According to recent research by BloombergNEF, electric cars and vans will be cheaper to produce than conventional, fossil fuel-powered vehicles by 2027 – only six years from now – even before any government subsidies.[5]

The rise of renewables

The energy sector is responsible for roughly three quarters of all greenhouse gas emissions.[6] Within it, the largest sources come from electricity and heat generation, followed by transportation and manufacturing.

According to the International Energy Agency (IEA) Global Energy Review 2021, electricity demand is heading for its fastest growth in more than ten years, and renewables are set to provide more than half of the increase in global electricity supply in 2021.[7] China alone is likely to account for almost half the global increase in renewable electricity generation.

The demand for renewables is expected to increase across all key sectors (power, heating, industry and transport), but particularly in the power sector.[8] In fact, renewables were the only energy source for which demand increased in 2020 despite the pandemic, with solar becoming in some places “the cheapest electricity in history.”[9] Annual renewable capacity additions in 2020 increased 45% to almost 280 GW. The IEA expects that the exceptionally high expansion of new renewable power capacity globally will become the “new normal” in 2021 and 2022.[10]

Last year also registered record-breaking competitive auctions for renewable contracts, as well as corporate renewable energy deals, with companies signing Power Purchase Agreements (PPAs) for nearly 25GW in 2020 – a 25% increase.

Putting all this renewable energy capacity to use requires massive investments in grid transmission lines, but can be helped with ongoing improvements in software technology to adjust power flow and grid enhancing technologies that avoid power bottlenecks.[11] The falling cost of batteries has already made a difference. Many scientists therefore expect that the clean energy transition may end up much cheaper than predicted.[12]

From the bottom-up: Market moves

Just a few months ago, in April 2021, RE100, the global initiative grouping businesses committed to 100% renewable electricity, saw a landmark of 300 companies join. Besides the goals of reducing emissions and improving customer satisfaction, what is driving this switch to 100% renewable electricity is cost savings.[13]

Companies under the RE100 group are also pushing the boundaries of energy procurement, with over a quarter of renewable power being sourced by members coming from PPAs that bring additional renewable energy to the grid.[14] Corporate PPAs, which speed up the deployment of renewable energy projects at guaranteed cost, have transformed power markets in the US, Europe and across Asia-Pacific in recent years.

Another example of the corporate advance is the growth of the Science Based Targets initiative (SBTi). According to the SBTi 2020 Progress Report, over 1,000 companies spanning 60 countries and nearly 50 sectors – including one-fifth of the Global Fortune 500 companies – are working with the SBTi to reduce their emissions.[15] In 2020, in spite of COVID-19, organizations joined the SBTi at an average rate of 31 companies a month.

More and more venture capital is also going to climate-tech start-ups.[16] Funds tracking the solar and wind industry consistently outperformed the S&P 500.[17] More recently, the Wall Street Journal reported that NextEra Energy (a Florida firm that sells wind and solar electricity to utilities) had become one of the most valuable energy companies in the world, its value rivaling that of Exxon and Chevron.[18] These days, there's apparently so much private equity and infrastructure fund action in the climate tech space that it's hard to keep up.[19]

Similar changes are taking place in the financial sector, where central banks have started to assume climate change as a financial and economic risk.[20]

While government regulation – or at least the expectation of it – is key, this decarbonization drive is now happening from the bottom-up.

From the top-down: The role of government and cross-border action

Still, all this market movement doesn’t completely replace the need for policy. Some of these changes are happening because investors expect policy to arrive. But taken together, they show a belief that the future is decarbonized — and that instead from damaging the economy, climate action could help it.

Fortunately for policy development and implementation, the COVID-19 pandemic made the importance of government intervention painfully clear.

At the international governance level, 2020 turned out to be a milestone year: before 2017 not a single G-20 country had pledged to reach net-zero emissions; now over 50 countries have done so. These pledges, together with those of hundreds of regions, cities and businesses, mean that net-zero climate goals now cover around 70% of global GDP and CO2 emissions.[21] While the assumptions that sustain some of these pledges are questionable, they have at least served to convey the direction in which we’re supposed to be going.

To accompany these commitments, some countries – including the EU, the US and Canada – have started to consider charging levies for carbon-intensive goods imported across their borders, particularly iron and steel, aluminum, cement, fertilizers and electricity.[22] Although these measures are certainly challenging to implement (beyond passing it through the World Trade Organization), it is not difficult to understand their logic and necessity: in a world of myriad climate policies and levels of ambition, they ensure that emission reductions are not evaded by simply crossing international borders, and protect national industry from being outcompeted by cheaper, carbon-intensive imports. In keeping with the green vortex idea, the mechanism has the potential to get exporting countries to reduce their own carbon emissions.[23]

The importance of China

In his speech to the UN General Assembly on September 2020, President Xi Jinping of China announced China’s goal to peak carbon dioxide emissions before 2030 and reach carbon neutrality before 2060. This would effectively be the biggest reduction of carbon intensity in the world and the fastest achievement of carbon neutrality after reaching emissions peak.

Indications that China is serious about its goals are many-fold. The country is expected to lead the world in renewable electricity growth in 2021, accounting for nearly half the world’s total.[24] In the past few months, it ratified the Kigali Amendment to the Montreal Protocol phasing out HFC gases[25] and launched its national emissions trading system – the largest carbon market in the world by volume.[26] And for the first time since its launch in 2013, China’s global infrastructure development strategy “Belt and Road Initiative” has not financed any coal projects in other countries in the first half of 2021, apparently as a result of new guidelines for greening overseas investment.[27]

More tellingly, to ensure that it meets its carbon peak and neutrality goals, China recently established a top-level climate “Leaders Group” comprised of the heads of the key national-level ministries and agencies.[28] The group is being led by China’s vice-premier and one of the most senior officials in the central government, Han Zheng. This sends out the message to China’s policymakers at all levels that the 2030 and 2060 targets are not to be taken lightly and that carbon neutrality is an economy-wide transformation.[29]

As stated by the WRI, “It is hard to overemphasize how transformational China’s carbon neutrality pledge is for international efforts to limit climate change. The Climate Action Tracker estimates that if China meets this target, it will lower global warming projections by around 0.2 to 0.3 degrees C. This pledge puts the world one big step closer to achieving the Paris Agreement's goals and avoiding the worst impacts of climate change.”[30]

In brief: 2050 is closer than 1990.

We know from experience that transformative, systemic change can happen quickly, in an exponential, non-linear manner. Changes that seemed implausible not long ago came to pass against all odds. In spite of the uncertainties of our time, there is little doubt that the decarbonization economy can provide steady, consistent opportunities for growth in the coming years. Like the digitization economy before it, once started, it’s not going away – especially not given the dire scientific predictions of unavoidable and irreversible climate change impacts that await us otherwise.

But will we move fast and decisively enough? To stay within somewhat safe limits we’re supposed to reach net-zero CO2 emissions by around 2050. We must remember: 2050 is already closer than 1990. And we might not be here in 2100, but our grandkids will.

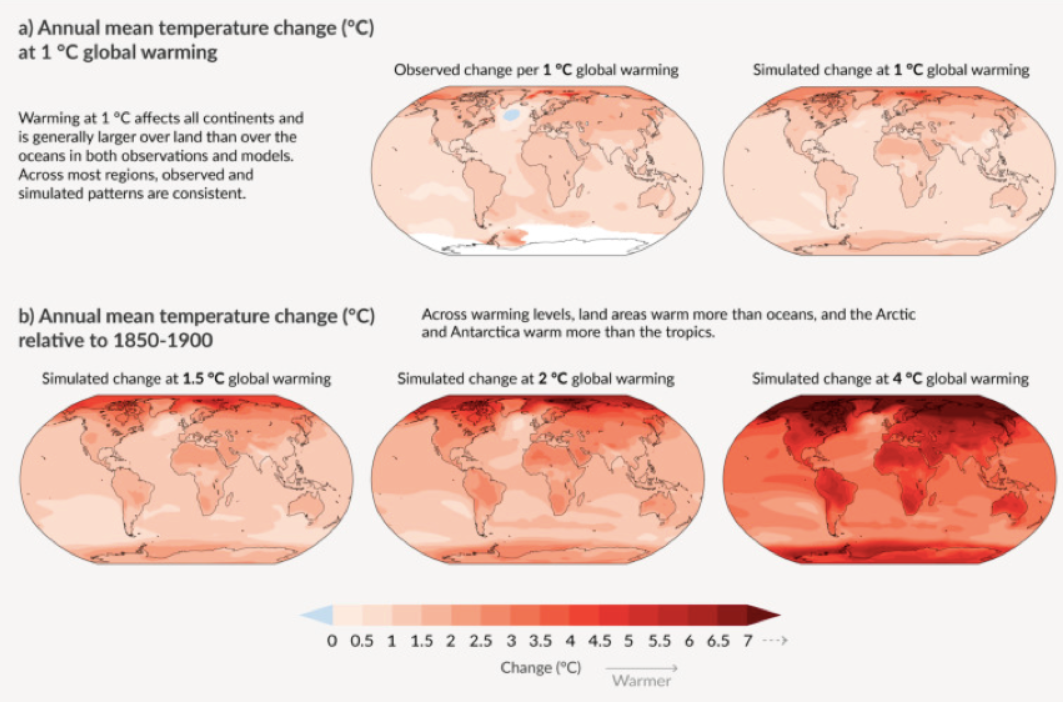

maria04_01Source: IPCC Working Group I, 2021.

Addendum

One of the most challenging points to convey when talking about climate change is the difference that an increase of one degree – or even half a degree – in global average temperatures makes, especially in terms of the impact this has at the local level. The recently released report by the Intergovernmental Panel on Climate Change (IPCC) summarizing the latest knowledge on the physical science basis of climate change includes a chart that shows this point for heatwave occurrence.[1] It shows, for example, how extreme heat events that used to occur once every 10 years will now (at current +1.2º C) occur 2.8 times every 10 years, and those that took place once every 50 years, now will do so 4.8 times in that period. With an increase of 1.5º C – which the IPCC report tells us we’ll reach in ca. 2040 – it will be 4.1 times for the once in a decade heatwave, and every 8.6 times for the once in five decades one. The frequency and also the intensity increase with every half degree.

maria04_02Source: IPCC Working Group I, 2021.

María Gutiérrez, Ph.D.

Consultant

International Institute for Sustainable Development (IISD)

United Nations Framework Convention on Climate Change (UNFCCC)

[10] このような数字をもってしても、IEAは再生エネルギーの役割を過小評価してきた経緯があります。2020年11月に発表された「IEA Renewables Report 2020」では、風力や太陽光の発電量が今後5年間で倍増し、ガスや石炭の発電量を上回り、2025年までに石炭を抜いて世界最大の電源になるとしていました。そのわずか6ヵ月後、同機関は風力・太陽光発電の世界的な成長率の予測をさらに25%上方修正しました。この修正には、政府の補助金を受けずに進めるプロジェクトが予想以上に多かった中国が大きく関係しています。Even with these numbers, the IEA has a history of underestimating the role of renewables. In November 2020, the IEA Renewables Report 2020 stated that wind and solar capacity would double over the next five years and exceed that of both gas and coal, displacing coal as the largest source of power worldwide by 2025. Only six months later, the agency had raised its forecast for the global growth of wind and solar by another 25%. The revised figure had to do largely with China, where more projects than expected were going ahead without government subsidies. See: https://www.iea.org/reports/renewable-energy-market-update-2021

[13] 昨年9月にRE100のメンバーを対象に行った調査では、回答者の約70%が100%再生可能エネルギーの電力に切り替える理由として、コスト削減を挙げています。A survey of RE100 members in September last year found that almost 70% of respondents cited cost saving as the driver for switching to 100% renewable electricity.

リスク管理やグリーン投資、低炭素投資に資本を動員することを目的としている「金融システムグリーン化ネットワーク」は、日本銀行や金融庁を含む95の中央銀行や金融監督機関がメンバーとなっています。As many as 95 central banks and financial supervisors (including the Bank of Japan and the Japan Financial Services Agency) are members of the Network for Greening the Financial System, with the stated goal of managing risk and mobilizing capital for green and low-carbon investments. See: https://www.ngfs.net/en

[21] EAの2021年版「2050年までにネットゼロを目指す。A roadmap for the global energy sector」 をご参照ください。See IEA’s 2021 “Net-zero by 2050: A roadmap for the global energy sector”

[25] HFCはある種の冷媒として使用され、地球温暖化係数(GWP)が二酸化炭素の1,000倍もあります。中国は世界最大のHFC製品の消費国および輸出国であり、世界の冷蔵庫の60%、家庭用エアコンの80%以上を占めています。モントリオール議定書のキガリ修正案では中国は2024年までにHFCの生産と使用を凍結し、2040年までにHFCの使用量を半減させることになっています。HFCs are used in certain types of refrigerants and have a global warming potential 1,000 times greater than carbon dioxide. China is the world’s largest consumer and exporter of HFC products, accounting for 60% of the world’s refrigerators and more than 80% of its residential air conditioners. Under the Kigali Amendment, China would freeze HFC production and use by 2024 and half HFC usage by 2040.

[29] さらに今年8月には、習近平国家主席が議長を務める政治局会議(中国共産党の最高意思決定機関)で、「2030年までを炭素排出量のピークとし、2060年までにカーボンニュートラルを達成する」という2つの目標を「協調的かつ秩序ある方法」で達成するよう、トップレベルの指示が出されました。This was followed in August this year with top-level instructions delivered at a Politburo meeting (the supreme decision-making body of the Communist Party of China) chaired by President Xi Jinping himself, where officials were urged to pursue the nation’s twin goals of reaching the carbon emission peak before 2030 and achieving carbon neutrality before 2060 in a “coordinated and orderly manner.” See: https://www.carbonbrief.org/china-issues-new-single-game-instructions-to-guide-its-climate-action